After reading the article included below, we couldn’t help but agree that the question every employer should be asking this year is…Should I self-fund my employee benefit plan?

As the article discusses, this is a great time of year for companies to review their status, evaluate changes that have been made and consider new items for their 2018 benefit to-do list. The article includes 8 questions benefits managers should be asking themselves this year. But, we’d like to help you address one key question – Is Self-Funding Right for You or Your Client?

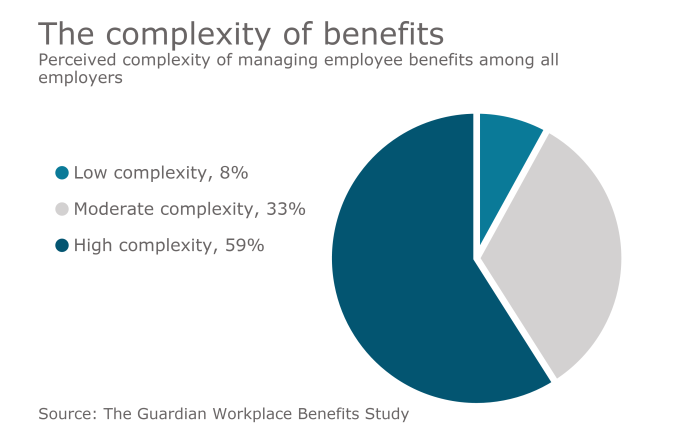

Whether you’ve been asking this question for some time or you’re new to the concept of self-funding, we’d be happy to explain the flexibility and potential for savings that a self-insured plan can offer. Gain control over your group health plan, eliminate the high costs of insurance premiums and obtain access to monthly claim reports – all with help from Diversified Group!

8 benefit management items to evaluate in 2018

This article was published on January 24, 2018 on Employee Benefit News, written by Zack Pace

Even 20 years into the benefits business, I still can’t always immediately remember details about my clients’ benefits plan — a given employer’s standard measurement period, affordability safe harbor or health savings account trustee, for example. That’s why I track all of these details across 32 columns in a simple spreadsheet.

While I use this reference tool most every day, I find that January is a great month to go even further with the employers I work with, carefully reviewing each company, considering how the employer’s circumstances have changed, and proposing items of consideration for our mutual 2018 benefit to-do list.

Employers are wise to have a similar benefit to-do list when it comes to their 2018 planning process. Here are eight common questions that benefits managers may find wise to ask.

1. For calendar year 2018, is your organization a “large employer” subject to ACA employer shared responsibility? Meanwhile, is your organization a “large employer” per your state’s fully insured group health plan market?

Generally, employers that averaged 50 or more full-time employees + full-time equivalents in calendar year 2017 are subject to ACA shared responsibility for all of calendar year 2018. Importantly, penalty risks generally now begin accruing in January, not when the plan year begins (if the date differs).

However, confusingly, in most states, the threshold to be considered a large employer for group health insurance contracts is an average of 51 or more full-time employee + full-time equivalents in the previous calendar year. How do the rules work in your state?

Now’s the time to finalize your 2017 calculation and determine your 2018 status for both employer shared responsibility and your state’s group health insurance market. And, yes, I’ve seen several employers average exactly 50 and be deemed a large employer regarding ACA employer shared responsibility and a small employer in reference to their fully insured group health plan contract. Talk about bad luck.

2. Is it time to self-fund the group medical plan?

The financial headwinds faced by fully insured plans have never been greater. Fully insured premiums are laden with the roughly 4% ACA premium tax (aka the Health Insurer Annual Fee), state premium taxes, the cost of various state-mandated benefits, and often robust retention and pooling point charges.

Thus, employers sponsoring group fully insured health plans should consider if moving to a self-funded contract (including so-called level-funding contracts) could be advantageous. Given the varying state regulations, state stop-loss minimums, organizational risk tolerance, reserve requirements and other variables, there is no one-size-fits-all answer to this question. Especially good times to perform a comprehensive self-funding evaluation are when your company crosses over from small group to large group and/or when meaningful claims experience becomes available from your fully insured vendor.

3. Is it time to self-fund the dental and short-term disability plans?

For most employers of size sponsoring plans that are not 100% employee paid (aka not voluntary), the answer to this question is simply “yes.” Run the math and make your decision.

4. Does benefit eligibility for life and disability vary by class?

For start-up companies, it’s not uncommon to offer better group life and disability benefits to certain classes, including management and executives. However, as employers grow, the budgetary and cultural reasons for doing so can quickly diminish or go away. A quick litmus test is simply asking yourself if the continuing benefit discrimination still makes sense.

Regardless if these benefits vary by class, is your group life plan compliant with the Section 79 nondiscrimination rules? Double-check with your attorney, accountant and benefits consultant.

5. Who is the health savings account trustee (i.e., the bank)? Is it linked to the health insurer?

If your organization sponsors a qualified high-deductible health plan, you likely allow employees to contribute to an HSA pre-tax through your Section 125 plan. Is the bank you selected still the best fit? Is the bank tied to your fully insured group health vendor? If yes, if you change your group health vendor, are your employees allowed to maintain the HSAs with this trustee with no fee changes? Should you consider moving to a quality stand-alone HSA vendor?

6. Does your firm employ anyone in California, Hawaii, New Jersey, New York, Rhode Island or Puerto Rico?

Most employers headquartered in these states (and territory) are acutely aware of the state disability requirements. However, given the advent of liberal telecommuting policies, it’s becoming more common for employers without physical locations in these states to employ individuals in these states. If you answered yes to this question, double-check your compliance with the state disability requirements. Your disability insurer or administrator can assist.

And, please note that, just this month (January 2018), New York became the latest state/jurisdiction to require paid family leave.

7. For firms offering retiree health plan benefits, are benefits for Medicare-eligible retirees and spouses self-funded?

While retiree health benefits have generally gone the way of the American chestnut tree, these benefits remain fairly common among certain sectors, such as higher education, government and certain nonprofits. Historically, most employers simply allowed Medicare-eligible retirees to remain on the employer’s active health plan, with the employer’s plan paying secondary to Medicare for Part A and Part B expenses and primary for prescription drug costs.

This arrangement was just fine when a really high annual prescription claim was $15,000. Now, $90,000 claims are not uncommon and $225,000 claims are possible. Does it still make sense to self-fund this retiree risk? In states where it is permissible, would it be prudent to transfer the risk by adopting a fully insured group Medicare Advantage plan or supplement program?

Regardless, all employers self-funding retiree health benefits should double-check that their individual stop-loss policy includes retirees.

And, regardless if retiree benefits are offered, all employers sponsoring self-funded health benefits should double-check that their individual stop-loss policy covers prescription drugs.

8. Is your firm required to file health and welfare Form 5550s? If so, who is handling the filings?

Generally, employers subject to ERISA that sponsor benefit plans that, at the beginning of the plan year, cover 100 or more participants, are required to file health and welfare 5500s and the related schedules. Some smaller employers must also file. Most multiple employer welfare arrangements (MEWAs) must file.

It’s very easy for health and welfare Form 5500 filing requirements to fall through the cracks. While U.S. Treasury’s penalties for non-filers are substantial, Treasury doesn’t keep track of who is required to file and thus doesn’t individually remind employers of this requirement. Further, this requirement doesn’t seem to be on the checklist of most auditors and accountants.

Employers should review all enrollment counts of all plans at the beginning of each year and consult with their accountant, attorney, and benefits consultant on the filing requirement and next steps.

I recommend avoiding the shortcut of saying “5500” in these discussions. Always say “the health and welfare 5500.” This practice will mitigate the risk that someone hears “5500” and thinks retirement plan 5500.

{kind=link}

{kind=link}

Leave A Comment