A recent Notes article from Employee Benefit Research Institute (ebri.org) examines 1996-2015 trends in self-insured health plans among private-sector establishments offering health plans and among their covered workers, with a particular focus on 2013 to 2015, so as to assess whether the Affordable Care Act (ACA) might have affected these trends. The data comes from the Medical Expenditure Panel Survey Insurance Component (MEPS-IC).

Self-Insured Health Plans: Recent Trends by Firm Size, 1996-2015

by Paul Fronstin, Ph.D., Employee Benefit Research Institute

Here are the key findings from the Employee Benefit Research Institute (EBRI):

- The percentage of private-sector establishments offering health plans at least one of which is self-insured has increased from 28.5% in 1996 to 39% in 2015 (36.8% increase).

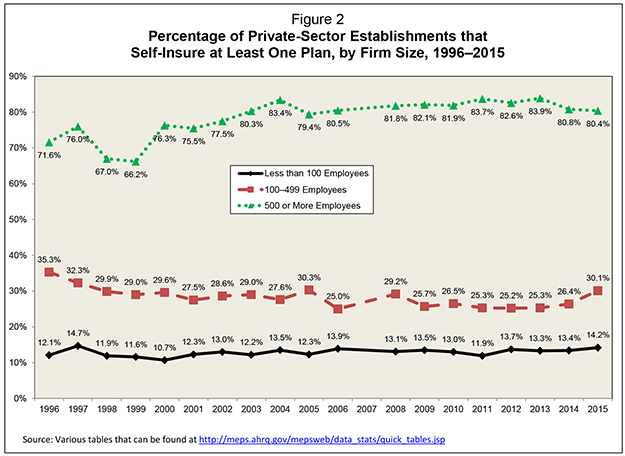

- Between 2013 and 2015, the percentages of establishments offering health plans with at least one self-insured plan has increased for midsized establishments from 25.3% to 30.1% (a 19% increase); for small establishments from 13.3% to 14.2% (a 7% increase); and has decreased from 83.9% to 80.4% for large establishments (a 4% decrease).

- Similarly, the percentage of health-plan-covered workers enrolled in self-insured health plans has increased from 58.2% to 60% (a 3% increase) from 2013 to 2015. The largest increases in self-insured plan coverage among covered workers have occurred in establishments with 25-99 employees and with 100-999 employees.

Introduction

Employment-based health plans generally fall into one of two categories―fully insured plans or self-insured plans. The key distinction is whether the employer has decided to purchase an insurance contract to cover the costs and financial risks associated with its employee health plan, or to use its own funds, including funds that might be set aside in a separate trust maintained by the employer (e.g., a voluntary employee beneficiary association) to cover such costs. Employers offering self-insured plans often purchase stop-loss coverage from an insurance company to mitigate against higher-than-budgeted expenses. Different experts may have different views about how any particular health plan should be classified, especially when plans include a flexible spending account (FSA), health reimbursement arrangement (HRA) or health savings account (HSA) that is funded separately from the main health plan.

The fully insured/self-insured distinction is also important from a legal perspective. Under the federal Employee Retirement Income Security Act of 1974 (ERISA), which provides the legal framework for the uniform provision of health benefits by employers doing business anywhere in the country, state laws (other than insurance laws) are generally pre-empted. This means, for example, that self-insured health plans do not have to satisfy state health insurance laws, including state-mandated reserve, benefit, claims, premium, and other requirements, which results in ease of administration and lower expenses. In contrast, fully insured plans are required (among other things) to cover state-mandated benefits and pay state insurance premiums. Both fully insured and self-insured health plans may have to comply with other federal laws applicable to such plans, such as components of the Affordable Care Act of 2010 (ACA).

Since the passage of the ACA, some commentators have speculated that an increasing number of small and midsized employers would convert their health plans from fully insured to self-insured plans.1 The rationale has appeared to be that several of the key ACA components—creditable coverage, affordability, essential benefits, and various taxes and fees—would drive up the cost of health coverage, thus possibly making self-insurance (which is viewed by many as generally less expensive than fully-insured alternatives) a more attractive option for many employers.

This EBRI Notes article examines recent trends in self-insured health plans among private-sector establishments and workers based on data from the Medical Expenditure Panel Survey Insurance Component (MEPS-IC). Data are presented in the aggregate and by establishment size. (2)

Establishments With Self-Insured Plans

The percentage of private-sector establishments offering health plans that report they self-insure at least one of their health plans has been generally increasing since at least the mid-1990s, well before passage of the ACA. In 2015, 39% of private-sector establishments reported that they self-insured at least one of their health plans, up from 28.5% in 1996 (a 36.8% increase) (Figure 1).

Over this same period, the portion of large establishments (those with 500 or more employees) offering health plans reporting they self-insure at least one plan has increased from 71.6% in 1996 to 80.4% in 2015, while the self-insured percentage for midsized establishments (100‒499 employees) with health plans has decreased from 35.3% to 30.1% over the period and for small establishments (fewer than 100 employees) has shifted from 12.1% to 14.2%. (Figure 2)

These long-term trends have generally held for each of the years during the period, until recently. Between 2013 and 2015, the percentage of establishments offering health plans with at least one self-insured plan increased for midsized establishments (from 25.3% to 30.1%), increased for small establishments (from 13.3% to 14.2%), but decreased for large establishments (from 83.9% to 80.4%).

Workers Enrolled in Self-Insured Plans

Consistent with the trend in the prevalence of self-insured plans among all establishments with at least one health plan, the percentage of covered workers (i.e., workers covered by an employment-based health plan) enrolled in self-insured plans has also been increasing. In 2015, 60 percent of covered workers were enrolled in self-insured plans, up from 46% in 1996 (Figure 3).

Similarly, over the 1996‒2015 period, the percentage of health-plan-covered workers employed by larger establishments (1,000 or more employees) and enrolled in self-insured plans has increased from 67% to about 86% (3), while the comparable self-insured percentage of workers (a) in midsized establishments (100‒999 employees) has shifted only from 39% to 40.5%, and (b) in smaller establishments (fewer than 100 employees) has shifted from only about 14% to 13% (Figure 4).

However, between 2013 and 2015, as a result of the increase in self-insured plans among small and midsized employers, the percentage of covered workers enrolled in self-insured plans increased from 58.2% to 60%. The largest increases in self-insured plan coverage among covered workers occurred in establishments with (a) 25‒99 employees, increasing from 13.2% to 15.2% (a 15% increase), and (b) 100‒999 employees, increasing from 33.6% to 40.5% (a 21% increase).

Conclusion

This EBRI Notes article describes trends in self-insured health plans among establishments of different employee sizes offering health plans and found that, between 2013 and 2015, the percentages of self-insured plans and of healthplan-covered workers in self-insured plans both increased among small and midsized establishments. These data are consistent with the perspective set forth above that the ACA would cause more small and midsized employers to adopt self-insured plans.

Endnotes

1. See, for example, comments made at the 2015 Sun Life Financial Wake Up Summit: http://www.sunlifesummit.com/, http://www.benefitspro.com/2013/08/06/self-insurance-a-threat-to-obamacare, and http://www.commonwealthfund.org/~/media/Files/Publications/Issue%20Brief/2012/Nov/1647_Buettgens_small_firm_self_insurance_under_ACA_ib.pdf

2. Self-reported data were examined from the Medical Expenditure Panel Survey Insurance Component (MEPS-IC), which is a survey of private- and public-sector employers fielded by the U.S. Census Bureau for the Agency for Healthcare Research and Quality (AHRQ). The survey has been fielded annually since 1996 (with the exception of 2007). Note that the survey collects data from private establishments, which consist of a single physical location. It is possible that some large employers are over-represented in the survey if more than one location was surveyed. Nearly 40,000 establishments were interviewed in 2015. See https://meps.ahrq.gov/mepsweb/survey_comp/ic_sample_size.jsp for more information.

3. Between 1996 and 1998, the share of self-insured workers for large employers dipped from 68.1 percent to 55.4 percent, but has steadily increased since then.

{kind=link}

{kind=link}

Leave A Comment