On June 19, 2018, the U.S. Department of Labor released the final rule on Association Health Plans (AHPs). The rule seeks to expand health coverage among small employer groups and self-employed individuals. It will make it easier for small business to join together to purchase health insurance without the myriad of regulations individual states and the Affordable Care Act (ACA) imposes on smaller fully insured employers. AHPs are not required to provide the essential health benefits (EHBs) package included in the ACA. The plans have been intended to provide less expensive options for small businesses, regional collectives, and industry groups that may not be able to purchase insurance through the public exchanges.

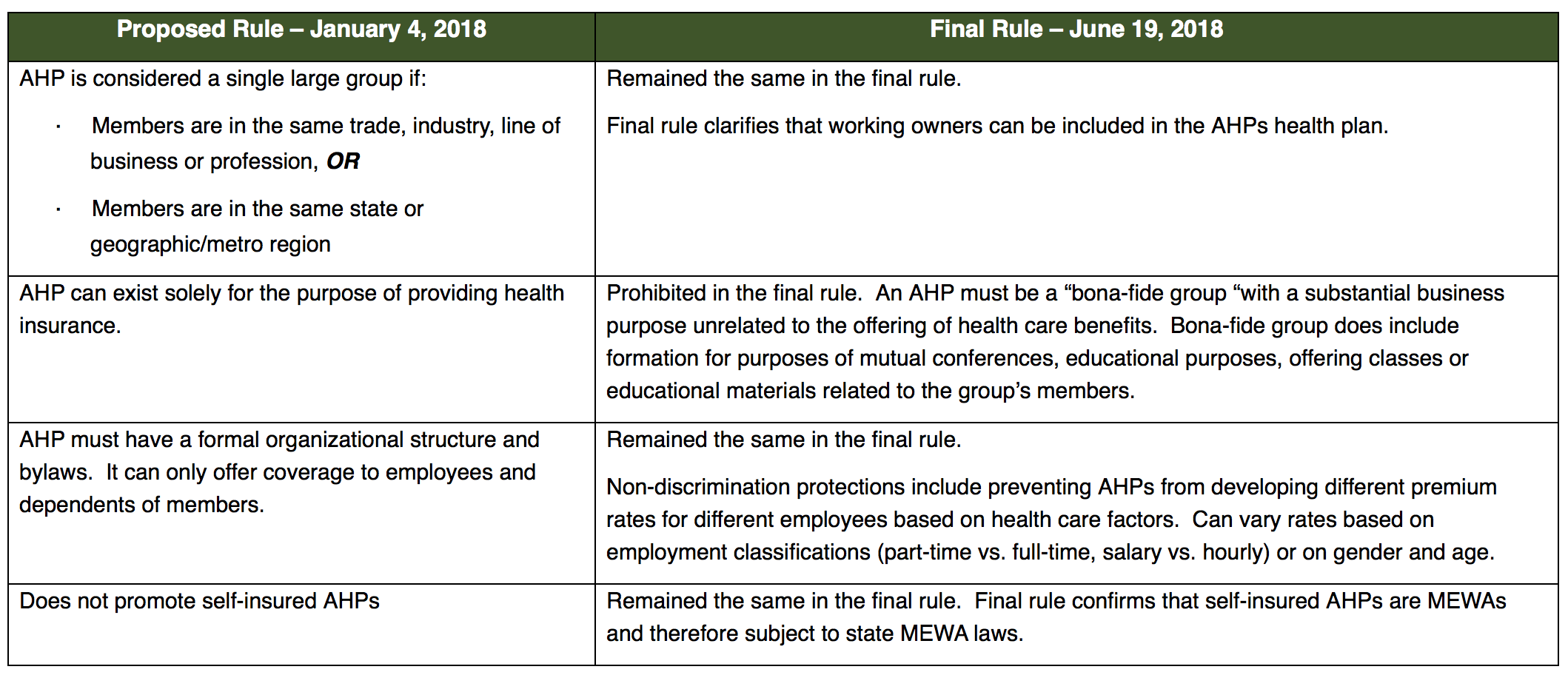

The rule broadens the definition of an employer under the Employee Retirement Income Security Act of 1974 (ERISA), to allow more groups to form association health plans and bypass rules under the Affordable Care Act. ERISA is the federal law that governs health benefits and retirement plans offered by large employers. Below is a comparison of the original proposed rule and the final rule just released.

The final rules confirm that self-insured Association Health Plans are considered Multiple Employer Welfare Arrangements (MEWAs) and does not curtail a state’s ability to regulate self-insured AHPs. This means that self-insured AHPs will be subject to MEWA laws in each state where coverage is offered/where members are located. Self-insured AHPs will have to follow the MEWA rules of the state with the most restrictive rule on an issue by issue basis. The final rule did leave an opening for future self-insured AHPs with the following language on page 96 of the 198 page regulation: “a potential future mechanism for preempting State insurance laws that go too far in regulating self-insured AHPs…” But for now, there is not anything in the final regulation designed to help self-insured AHPs thrive.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment