This article appeared on Kaiser Family Foundation on September 19, 2017.

Employer-sponsored insurance covers over half of the nonelderly population; approximately 151 million non-elderly people in total.1 To provide current information about employer-sponsored health benefits, the Kaiser Family Foundation (Kaiser) and the Health Research & Educational Trust (HRET) conduct an annual survey of private and nonfederal public employers with three or more workers. This is the nineteenth Kaiser/HRET survey and reflects employer-sponsored health benefits in 2017.

HEALTH INSURANCE PREMIUMS AND WORKER CONTRIBUTIONS

In 2017, the average annual premiums for employer-sponsored health insurance are $6,690 for single coverage and $18,764 for family coverage [Figure A]. The average single premium increased 4% and the average family premium increased 3% in 2017. Workers’ wages increased 2.3% and inflation increased 2.2% over the last year.2 The average premium for family coverage is lower for covered workers in small firms (3-199 workers) than for workers in large firms (200 or more workers) ($17,615 vs. $19,235).

Premiums for family coverage have increased 19% since 2012 and 55% since 2007. Average premiums for high-deductible health plans with a savings option (HDHP/SOs) are considerably lower than the overall average for all plan types for both single and family coverage, at $6,024 and $17,581, respectively [Figure A]. These premiums do not include any firm contributions to workers’ health savings accounts or health reimbursement arrangements.

Premiums vary significantly around the averages for both single and family coverage, reflecting differences in health care costs and compensation decisions across regions and industries. Seventeen percent of covered workers are in plans with an annual total premium for family coverage of at least $22,517 (120% or more of the average family premium), and 21% of covered workers are in plans where the family premium is less than $15,011 (less than 80% of the average family premium).

Most covered workers make a contribution toward the cost of the premium for their coverage. On average, covered workers contribute 18% of the premium for single coverage and 31% of the premium for family coverage. Workers in small firms contribute a higher average percentage of the premium for family coverage than workers in large firms (39% vs. 28%).

Covered workers in firms with a relatively high percentage of lower-wage workers (at least 35% of workers earn $24,000 a year or less) contribute higher percentages of the premium for single (23%) and family (37%) coverage than workers in firms with a smaller share of lower-wage workers (18% and 31%, respectively).3

As with total premiums, the share of the premium contributed by workers varies considerably. For single coverage, 14% of covered workers are in plans that do not require them to make a contribution, 60% are in plans that require a contribution of 25% or less of the total premium, and 2% are in plans that require a contribution of more than half of the premium. For family coverage, 3% of covered workers are in plans that do not require them to make a contribution, 44% are in a plan that requires a contribution of 25% or less of the total premium, and 16% are in plans that require more than half of the premium. Covered workers in small firms are more likely than covered workers in large firms to be in a plan that requires the worker to contribute more than 50% of the total family premium (36% vs. 8%).

With regard to dollar amounts, the average annual premium contributions by covered workers for 2017 are $1,213 for single coverage and $5,714 for family coverage. Eight percent of covered workers contribute $12,000 or more a year for family coverage. Average contribution amounts for covered workers in HDHP/SOs are lower for single and family coverage than for covered workers in other plan types [Figure A]. Covered workers’ average dollar contribution to family coverage has increased 74% since 2007 and 32% since 2012. Covered workers in small firms have lower average contributions for single coverage than workers in large firms ($1,030 vs. $1,289), but higher average contributions for family coverage ($6,814 vs. $5,264).

One reason for this variation in dollar amounts is the different approaches that employers use to structure employee contributions, particularly for family coverage. Of firms that offer family coverage, 45% of small firms and 15% of large firms provide the same dollar contribution for single and family coverage, which means that workers must pay the full additional premium cost to enroll family members in their plan. Forty-five percent of small firms and 75% of large firms make a higher dollar contribution for family coverage than for single coverage; 1% of small firms and 4% of large firms vary their approach with the class of the employee; and the remaining 9% of small firms and 6% of large firms take some other approach. Sixteen percent of covered workers are in a plan that requires workers who use tobacco to contribute more toward the premium.

Figure A: Average Annual Firm and Worker Premium Contributions and Total Premiums for Covered Workers for Single and Family Coverage, by Plan Type, 2017

PLAN ENROLLMENT

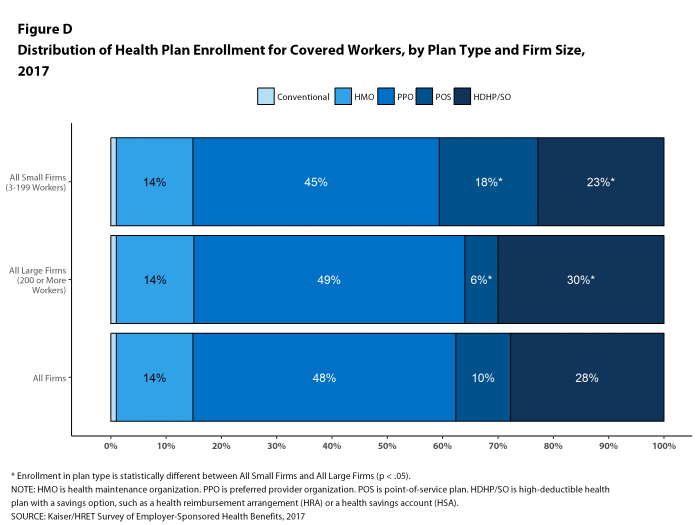

PPOs continue to be the most common plan type in 2017, enrolling 48% of covered workers. Twenty-eight percent of covered workers are enrolled in a high-deductible plan with a savings option (HDHP/SO), 14% in an HMO, 10% in a POS plan, and <1% in a conventional (also known as an indemnity) plan [Figure D]. Over the last five years, enrollment in PPOs has fallen by 8 percentage points while enrollment in HDHP/SOs has increased by 9 percentage points. Six percent of firms offering an HDHP/SO offer only an HDHP/SO to at least some of their workers.

Figure D: Distribution of Health Plan Enrollment for Covered Workers, by Plan Type and Firm Size, 2017

Self-Funding. Fifteen percent of covered workers in small firms and 79% in large firms are enrolled in plans that are either partially or completely self-funded, similar to last year. Although there has been discussion of more insurers offering partially self-funded plans (sometimes called level-premium plans) to smaller employers, we have not seen an increase in respondents reporting that they have self-funded plans in recent years.

Association Health Plans. Six percent of offering firms with fewer than 250 workers offer health benefits arranged through a trade or professional association.

EMPLOYEE COST SHARING

Most covered workers must pay a share of the cost when they use health care services. Eighty-one percent of covered workers have a general annual deductible for single coverage that must be met before most services are paid for by the plan [Figure E]. Even workers without a general annual deductible often face other types of cost sharing when they use services, such as copayments or coinsurance for office visits and hospitalizations.

Among covered workers with a general annual deductible, the average deductible amount for single coverage is $1,505, similar to the average deductible last year ($1,478). The average deductible for covered workers is higher in small firms than in large firms ($2,120 vs. $1,276). Among all covered workers, including both those with and without a deductible, the average deductible is $1,221. Fifty-eight percent of covered workers in small firms and 48% of covered workers in large firms are in a plan with a deductible of at least $1,000 for single coverage, similar to the percentages last year. Over the last five years, however, the percentage of covered workers with a general annual deductible of $1,000 or more for single coverage has grown substantially, increasing from 34% in 2012 to 51% in 2017 [Figure E]. Thirty-seven percent of covered workers in small firms are in a plan with a deductible of at least $2,000, compared to 15% for covered workers in large firms.

Deductibles have increased in recent years due to higher deductible amounts within plan types and to higher enrollment in HDHP/SOs. While growing deductibles in PPOs and other plan types generally increase enrollee out-of-pocket liability, the shift in enrollment to HDHP/SOs does not necessarily do so because most HDHP/SO enrollees receive an account contribution from their employers. Twenty-one percent of covered workers in an HDHP with a Health Reimbursement Arrangement (HRA) and 2% of covered workers in a Health Savings Account (HSA)-qualified HDHP receive an account contribution for single coverage at least equal to their deductible, while another 35% of covered workers in an HDHP with an HRA and 30% of covered workers in an HSA-qualified HDHP receive account contributions that, if applied to their deductible, would reduce their cost sharing to less than $1,000.

Whether they face a general annual deductible or not, a large share of covered workers also pay a portion of the cost when they visit an in-network physician. For primary care, 71% of covered workers have a copayment (a fixed dollar amount) when they visit a doctor and 22% have coinsurance (a percentage of the covered amount). For specialty care, 67% face a copayment and 26% face coinsurance. The average copayments are $25 for primary care and $38 for specialty care. The average coinsurance is 19% for primary and 19% for specialty care. These amounts are similar to those in 2016.

Most workers also face additional cost sharing for an emergency room visit, hospital admission, or outpatient surgery. After any general annual deductible is met, 32% of covered workers have a coinsurance and 58% have a copayment for an emergency room visit, and 64% of covered workers have a coinsurance and 12% have a copayment for hospital admissions. The average coinsurance rate for hospital admissions is 19% and the average copayment is $336 per hospital admission. The cost sharing provisions for outpatient surgery follow a similar pattern to those for hospital admissions.

While almost all (98%) covered workers are in plans with a limit on in-network cost sharing (called an out-of-pocket maximum) for single coverage, there is considerable variation in the actual dollar limits [Figure F]. Fifty-seven percent of these workers are in a plan with an annual out-of-pocket maximum for single coverage of more than $3,000, while 18% are in a plan with an out-of-pocket maximum of $6,000 or more.

Figure E: Percentage of Covered Workers With Various Single Coverage General Annual Deductible Levels, 2012 and 2017

Figure F: Percentage of Covered Workers Enrolled In a Plan With an Out-Of-Pocket Maximum for Single Coverage, 2009-2017

AVAILABILITY OF EMPLOYER-SPONSORED COVERAGE

Fifty-three percent of firms offer health benefits to at least some of their workers, similar to the percentage last year [Figure G]. Eighty-nine percent of workers are in a firm that offers health benefits to at least some of its workers. Over the past decade, the percentage of workers at small firms that offer health benefits to at least some workers has decreased (78% vs 73%).

The likelihood of offering health benefits differs significantly by firm size, with only 40% of firms with 3 to 9 workers offering coverage while virtually all firms with 1,000 or more workers offer coverage.

Even in firms that offer health benefits, some workers are not eligible to enroll (e.g., waiting periods or part-time or temporary work status) and others who are eligible choose not to enroll (e.g., they feel the coverage is too expensive or they are covered through another source). In firms that offer coverage, 79% of workers are eligible for the health benefits offered, and of those eligible, 78% take up the firm’s offer, resulting in 62% of workers in offering firms enrolling in coverage through their employer. All of these percentages are similar to 2016.

Looking across workers both in firms that offer and those that do not offer health benefits, 55% of workers are covered by health plans offered by their employer.

Coverage for Family Members. Among firms offering health benefits, virtually all large firms and 94% of small firms offer coverage to spouses of eligible workers. Similarly, virtually all large firms and 92% of small firms offering health benefits offer coverage to other dependents of their eligible workers, such as children.

Figure G: Percentage of Firms Offering Health Benefits, by Firm Size, 1999-2017

RETIREE COVERAGE

Of the large firms offering health benefits to workers in 2017, 25% also offer health benefits to retirees, similar to the percentage in 2016 (24%). Among large firms that offer retiree health benefits, 95% offer health benefits to early retirees (workers retiring before age 65) and 66% offer health benefits to Medicare-age retirees. Twenty-six percent of large firms offering retiree benefits contribute to benefits through a contract with a Medicare Advantage plan. Twelve percent of large firms offering retiree benefits offer retiree benefits through a corporate or private exchange.

SUPPLEMENTAL AND VOLUNTARY BENEFITS

Firms offering health benefits also offer a variety of supplemental and other health benefits to their workers. Among firms offering health benefits, 67% of small firms and 97% of large firms offer dental benefits to their workers; 47% of small firms and 82% of large firms offer vision benefits; 23% of small firms and 46% of large firms offer critical illness insurance; 16% of small firms and 28% of large firms offer hospital indemnity insurance; and 16% of small firms and 25% of large firms offer long-term care insurance. Among all firms offering these supplemental benefits, firms are more likely to make a contribution toward dental coverage (67%) or vision coverage (54%) than for critical illness insurance (3%) or hospital indemnity insurance (5%).

WELLNESS, HEALTH RISK ASSESSMENTS AND BIOMETRIC SCREENINGS

A large share of firms have programs that encourage workers to identify health issues and to take steps to improve their health. Many firms offer health screening programs including health risk assessments, which are questionnaires asking workers about lifestyle, stress or physical health, and in-person examinations such as biometric screenings. Many firms also use incentives to encourage workers to complete assessments, participate in wellness programs, or meet biometric outcomes. As we have seen in previous years, there is considerable uncertainty among small firms on some questions, particularly those related to incentives, so findings are reported only for large firms in some instances.

Health Risk Assessments. Among firms offering health benefits, 38% of small firms and 62% of large firms provide workers an opportunity to complete a health risk assessment. A health risk assessment includes questions about a person’s medical history, health status, and lifestyle. Fifty-two percent of large firms with a health risk assessment program offer an incentive to encourage workers to complete the assessment. Among large firms with an incentive, the incentives include: gift cards, merchandise or similar incentives (50% of firms); requiring a completed health risk assessment to be eligible for other wellness incentives (46% of firms); lower premium contributions or cost sharing (46% of firms); and financial rewards such as cash, contributions to health-related savings accounts, or avoiding a payroll fee (40% of firms).

Biometric Screenings. Twenty-one percent of small firms and 52% of large firms offering health benefits offer workers the opportunity to complete a biometric screening. A biometric screening is a health examination that measures a person’s risk factors such as body weight, cholesterol, blood pressure, stress, and nutrition. Fifty-three percent of large firms with biometric screening programs offer workers an incentive to complete the screening. Among large firms with an incentive, the incentives include: lower premium contributions or cost sharing (49% of firms); gift cards, merchandise or similar incentives (44% of firms); requiring a completed biometric screening to be eligible for other wellness incentives (41% of firms); and financial rewards such as cash, contributions to health-related savings accounts, or avoiding a payroll fee (33% of firms). In addition, 14% of large firms with a biometric screening program have incentives tied to whether workers met specified biometric outcomes, such as a targeted body mass index (BMI) or cholesterol level.

Health and Wellness Promotion Programs. Many firms offer programs to help workers identify health risks and unhealthy behaviors and improve their lifestyles. Fifty-eight percent of small firms and 85% of large firms offer a program in at least one of these areas: smoking cessation; weight management; behavioral or lifestyle coaching. Thirty-two percent of large firms with one of these health and wellness programs offer workers an incentive to participate in or complete the program. Among large firms with an incentive for completing wellness programs, incentives include: gift cards, merchandise or similar incentives (68% of firms); requiring completion of activities to be eligible for other wellness incentives (44% of firms); financial rewards such as cash, contributions to health-related savings accounts, or avoiding a payroll fee (37% of firms); and lower premium contributions or cost sharing (19% of firms).

Eight percent of small firms and 14% of large firms report collecting health information from workers through wearable devices such as a Fitbit or Apple Watch.

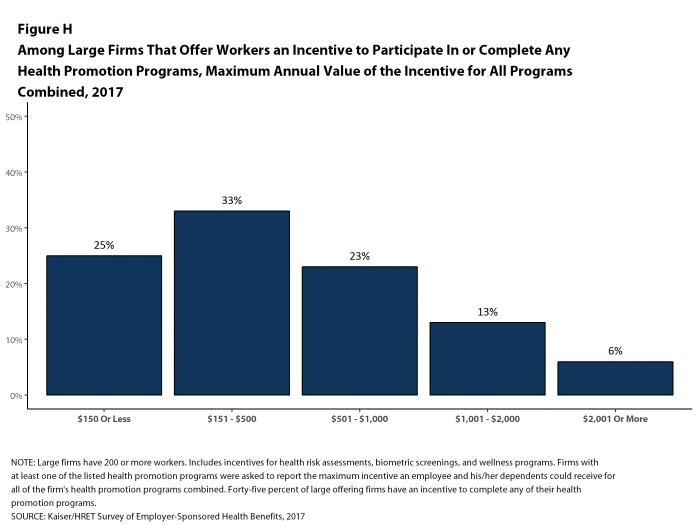

As risk assessments and wellness programs have become more complex, incentives and rewards have become more sophisticated and may involve participating in or meeting goals in different programs (e.g., completing an assessment and participating in a health promotion activity). To better understand the combined incentives or penalties facing program participants, we asked large firms that had any incentives for health risk assessments, biometric screenings, or the specified health and wellness promotion programs what the maximum incentive was for a worker for all of their programs combined. Among large firms with any type of incentive, 25% have a maximum incentive of 150 or less; 33% have a maximum incentive between $151 and $500; 23% have a maximum incentive between $501 and $1,000; 13% have a maximum incentive between $1,001 and $2,000; and 6% have a maximum incentive of more than $2,000 [Figure H].

Figure H: Among Large Firms That Offer Workers an Incentive to Participate In or Complete Any Health Promotion Programs, Maximum Annual Value of the Incentive for All Programs Combined, 2017

SITES OF CARE

Telemedicine. Sixty-three percent of large firms that offer health benefits cover the provision of health care services through telecommunication in their largest health plan [Figure I]. Among these firms, 33% reported that workers have a financial incentive to receive services through telemedicine instead of visiting a physician’s office.

Retail Health Clinics. Seventy-three percent of large firms cover services offering health benefits provided in retail health clinics, such as those found in pharmacies and supermarkets, in their largest health plan [Figure I]. Among these firms, 17% reported that workers have a financial incentive to receive services in a retail clinic instead of visiting a traditional physician’s office.

Nurse Hotline. Seventy-nine percent of large firms offering health benefits have a nurse hotline as part of their largest health plan [Figure I].

PROVIDER NETWORKS

High Performance or Tiered Networks. Fifteen percent of large firms offering health benefits have high performance or tiered networks in their largest health plan, similar to the percentage reported last year [Figure I]. These programs identify providers that are more efficient and generally provide financial or other incentives for enrollees to use the selected providers.

Narrow Networks. Nine percent of large firms offering health benefits offer a health plan that they consider to have a narrow network (i.e., a network they would consider more restrictive than a standard HMO network), similar to the percentage reported last year [Figure I].

Eliminated Hospitals or Health Systems. Only 3% of large firms report that they or their health plan eliminated a hospital or health system in the past year in order to reduce the costs of their plan, similar to the percentage reported last year [Figure I].

Figure I: Among Large Firms Offering Health Benefits, Percentage of Firms Whose Plan Includes Various Features, 2017

Private Exchanges. Four percent of firms offering health benefits with at least 50 workers offer health benefits through a private exchange. Among firms offering health benefits that do not currently offer through a private exchange, 10% with at least 50 workers, including 22% with at least 5,000 workers, say they have considered offering coverage through a private exchange.

CONCLUSION

The market for employer-sponsored health benefits continues along with no big changes in 2017. Premium increases are modest and there is no appreciable change in cost sharing or enrollment by type of plan. Employers continue to invest in health promotion and wellness approaches, including building incentives around programs that collect information about employee health and lifestyles.

Despite continuing economic improvement, with lower rates of unemployment, and the ACA employer mandate, there are no signs that the long-term declines in the offer and coverage rates are reversing. Even with modest premium growth, offer rates for small firms remain much lower than those for large firms, and the percentage of workers covered at work remains at 62%.

We continue to see significant variation around the average premiums and contribution amounts, particularly for small businesses. A meaningful share of covered workers in small firms must pay a substantial share of the cost of family coverage, raising the question of whether this is a viable source of coverage for the dependents of these workers.

The debate about the future of the ACA has focused on the provisions that extended coverage in the non-group market and Medicaid, with the provisions affecting employer-sponsored coverage receiving relatively little attention. Employers generally appear to have adapted to ACA provisions without significant disruption, including the employer requirement to offer coverage or pay a penalty, the provisions requiring preventive care be covered without cost sharing, and that non-grandfathered plans have an out-of-pocket limit on cost sharing. Even if repeal and replace efforts ultimately succeed, the impacts on the group market will likely be relatively small: for example, some employers may reduce offers of coverage to some of their lower-paid employees or may reduce the number of preventive services available without cost sharing; but the larger metrics measuring costs and coverage are unlikely to change in any significant way.

One policy that could affect the market over the next couple of years is the high-cost plan tax, also known as the Cadillac tax. In previous surveys, employers reported increasing cost sharing and making other changes in anticipation of the high-cost plan tax taking effect in 2018. With the effective date of the tax delayed until 2020 (and with the apparent widespread Congressional support for further delay), the pressure for employers with more expensive plans to take actions to reduce their cost seems to have abated. This could change abruptly, however, if the tax is not further delayed in the near future.

METHODOLOGY

The Kaiser Family Foundation/Health Research & Educational Trust 2017 Annual Employer Health Benefits Survey (Kaiser/HRET) reports findings from a telephone survey of 2,137 randomly selected non-federal public and private employers with three or more workers. Researchers at the Health Research & Educational Trust, NORC at the University of Chicago, and the Kaiser Family Foundation designed and analyzed the survey. National Research, LLC conducted the fieldwork between January and June 2017. In 2017, the overall response rate is 33%, which includes firms that offer and do not offer health benefits. Among firms that offer health benefits, the survey’s response rate is also 33%. To improve estimates for small firms, the 2017 survey had a significantly larger sample than previous years; the increased sample size lead to both more firms completing the survey and a lower response rate than in years past. Unless otherwise noted, differences referred to in the text and figures use the 0.05 confidence level as the threshold for significance.

For more information on the survey methodology, please visit the Methodology section at http://ehbs.kff.org/.

- Kaiser Commission on Medicaid and the Uninsured. The uninsured: A primer — Key facts about health insurance and the uninsured in the era of health reform: Supplemental Tables [Internet]. Washington (DC): The Commission; 2016 Nov [cited 2017 Aug 1]. http://files.kff.org/attachment/Supplemental-Tables-The-Uninsured-A%20Primer-Key-Facts-about-Health-Insurance-and-the-Unisured-in-America-in-the-Era-of-Health-Reform. See Table 1: 271.3 million nonelderly people, 55.8% of whom are covered by employer-sponsored insurance.↩

- Kaiser/HRET surveys use the April-to-April time period, as do the sources in this and the following note. The inflation numbers are not seasonally adjusted. Bureau of Labor Statistics. Consumer Price Index – All Urban Consumers: Department of Labor; 2017. [cited 2017 July 21] https://data.bls.gov/timeseries/CUUR0000SA0?output_view=pct_1mth. Wage data are from the Bureau of Labor Statistics and based on the change in total average hourly earnings of production and nonsupervisory employees. Employment, hours, and earnings from the Current Employment Statistics survey: Department of Labor; 2017 [cited 2017 July 21]. http://data.bls.gov/timeseries/CES0500000008↩

- This threshold is based on the twenty-fifth percentile of workers’ earnings as reported by the Bureau of Labor Statistics, using data for 2016. Bureau of Labor Statistics. May 2016 national occupational employment and wage estimates: United States [Internet]. Washington (DC): BLS; [last modified 2017 Mar 310; cited 2017 Aug 15]. Available from: http://www.bls.gov/oes/current/oes_nat.htm↩

{kind=link}

{kind=link}

Leave A Comment